The desire for traders to have lower execution prices and extra anonymity is what bred the creation of dark Initial exchange offering swimming pools. Exchange-owned darkish pools embody those offered by NYSE Euronext, BATS Trading, and London Inventory Exchange’s Turquoise. Darkish swimming pools are often solely accessible to institutional investors, leaving smaller investors at a disadvantage. One Other example of dark pool trading coming beneath regulatory scrutiny is the case involving Funding Technology Group (ITG) in 2015.

Like the dealer-owned pools, these platforms act on a proprietary capability. A darkish pool is a privately held change where large companies and institutional buyers commerce large shares of securities with out disclosing them to public markets. Therefore, so as to avoid excessive market swings and attainable manipulation, investment banks and large financial firms created non-public exchanges. These closed marketplaces have less transparency to mitigate their impacts on market prices, therefore the name of darkish pools. HFT-powered programs use algorithms-based models to execute trades multiple trades virtually instantaneously.

Worth discovery is the process by which the market determines the fair value of an asset based on supply and demand. Critics argue that darkish swimming pools undermine price discovery by siphoning off a good portion of buying and selling exercise from public exchanges. Trades inside darkish swimming pools are matched internally, typically using algorithms. For a commerce to be considered for dark pools, it should meet sure amount thresholds. The minimal block dimension necessities are outlined beneath ICE Swap Commerce Rulebook. Given the large volumes of contracts, block traders typically negotiate for higher prices — only https://www.xcritical.in/ giant financial establishments like hedge funds, insurance providers, and pension funds.

However they have higher fees and commissions, restricted proprietary merchandise, less evaluation and analysis, and fewer personalized service. They cater to their clients and permit them to trade immediately in opposition to the firm’s proprietary trading desks and consumer order flows, offering liquidity and potential price savings. Examples embrace Credit Score Suisse’s CrossFinder and Goldman Sachs‘ Sigma X. By keeping their trades hidden, they’ll avoid price movements that happen when the market learns of a large purchase or sell order.

Therefore, a retail investor usually has little use for darkish pool trading regardless of its surge in popularity. However, darkish pool trading just isn’t popular in India as rules ask for all trades to be reported on an trade platform. Compared to the US, Canada has a better level of transparency surrounding market trading volumes. An example of darkish pool trading could be an institutional investor, similar to Warren Buffet, buying shares in a company like Tesla.

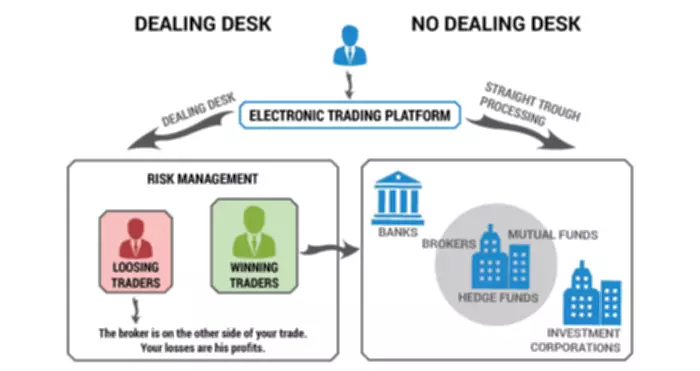

Company Broker Or Exchange-owned Darkish Pool

The first kind of dark pool is the one offered by broker-dealers, who engage in monetary markets to develop their very own wealth in addition to executing trades on behalf of their shoppers to earn some commissions. Let’s shed some light on darkish pool buying and selling and if there are any advantages to these private liquidity pools. There’s no practical chance that a median retail dealer will shift the market. Unless you handle a considerable portfolio, your affect in the marketplace most probably isn’t going to drastically influence other investors.

List Of Darkish Swimming Pools

It is fascinating (and perhaps frightening) to note that darkish swimming pools account for a good portion of day by day trading volume in U.S. equity markets. In current years this was estimated to vary between 15% and 20% of all trading quantity. However on January 24, 2005 Bloomberg revealed that for the first time in historical past, “off-exchange activity is on course to account for a document 51.8% of traded volume.” The a part of the market construction adds to the efficiency of the stock market by providing liquidity of certain securities. Darkish pools have turn out to be so prevalent that just about 40% of all executed stock trades in the U.S are done in dark pools.

Though many darkish pools are registered with monetary authorities, regulators nonetheless act with more suspicion in terms of these opaque liquidity pools. Usually speaking, exchanges are handled extra favorably by authorities, who’re keen to maintain the enjoying subject as clear as attainable. Darkish pool caters to their curiosity because the retail traders are completely oblivious to the execution particulars of the large trade.

- However, as a retail dealer, you likely won’t be buying and selling with the volumes seen in block buying and selling, which means that the anonymity gained from darkish pool buying and selling is unlikely to be useful.

- The markets obtained a glimpse of Algo trading’s manipulative effect in the “Flash Crash” of 2010, caused by illegal spoofing and layering.

- Dark swimming pools could deliver several indirect benefits for retail investors, there is the potential for exploitation of users by additional technologically superior gamers.

- ECN networks had been initially utilized by brokers to execute trades on behalf of their clients.

In April 2019, the share of U.S. stock trades executed on darkish swimming pools and different off-market autos was nearly 39%, in accordance with a Wall Avenue Journal report. Light pool buying and selling is the opposite of darkish pool trading, using ‘lit pools’ that have a public order guide. This means gentle pool merchants can use the bid and offer info obtainable in the order book to predict market developments. Dark pool trading can be accessed through brokers similar to Goldman Sachs’ Sigma X, stock exchanges corresponding to Liquidnet, or particular person darkish pool corporations similar to Knight Capital Group. Broker-dealer-owned darkish swimming pools are constructed by broker-dealers looking to present their shoppers with dark-pool options. Examples of such darkish swimming pools embrace CrossFinder from Credit Score Suisse, Sigma X from Goldman Sachs, and MS Pool from Morgan Stanley.

A few examples of this dark pool are Credit Score Suisse’s CrossFinder, Morgan Stanley’s M.S. Pool, JPMorgan Chase, and Barclays Capital. Though there’s lots of ambiguity round Dark pool trading, they are regulated underneath the Regulation ATS of 1998. This regulation launches a two-tier system for various trading techniques. Under this, ATSs have the choice to register as broker-dealers or as nationwide securities exchanges, with minimal compliance reporting. In the present scenario, Dark Pools’ prominence has increased greater than ever earlier than. Darkish Swimming Pools came into existence to deal with the need of the large institutional buyers or merchants.

Darkish swimming pools usually are not required to reveal their buying and selling volumes or the individuals of their trades to the common public darkpool, making it difficult for regulators to observe them. Critics argue that darkish swimming pools contribute to market fragmentation and reduce transparency, making it more durable for regulators to observe trades and ensure that markets are honest. They additionally raise considerations about conflicts of interest, since some dark pools are owned by the identical firms that commerce inside them.

They would then swiftly purchase the inventory before you are in a position to, and promote it to you at a higher worth. For instance, if Company ABC has a bid of $119/share, and asks of $121/share, the common market worth would be $120, which is what institutions ought to trade at inside dark swimming pools. A regulatory change by the Securities and Exchange Commision (SEC) in 1979 incepted the concept of dark swimming pools.